Growing a SaaS business in 2024 is increasingly complex from a tax perspective. Governments around the world are rapidly evolving their sales tax and VAT obligations for digital businesses, making it harder and harder to keep up.

Whether you’re just starting your business or looking toward an exit, here are the key sales tax and VAT milestones.

Startup: less than $5M in revenue

With all the moving pieces of starting a new company, sales tax is probably not on your radar from day one. But there are a few key milestones to look out for in order to avoid paying out-of-pocket expenses down the road.

Hiring your first employees

If you have an employee in a US state, you’re obligated to comply with any sales tax regulations in that jurisdiction. So if any of your first hires are in a state that taxes software products, you’ll need to go ahead and register to collect sales tax with local authorities.

Making your first sales

Depending on the product you’re selling and where your customers are located, you could be on the hook for sales tax or VAT from your very first sale. Taking a few key steps can help you stay ahead of any liability:

- Collect the right customer data: Knowing your customers’ locations and tax statuses is the first step to compliance. Make sure you’re capturing accurate address information and, for international customers, VAT IDs, from day one.

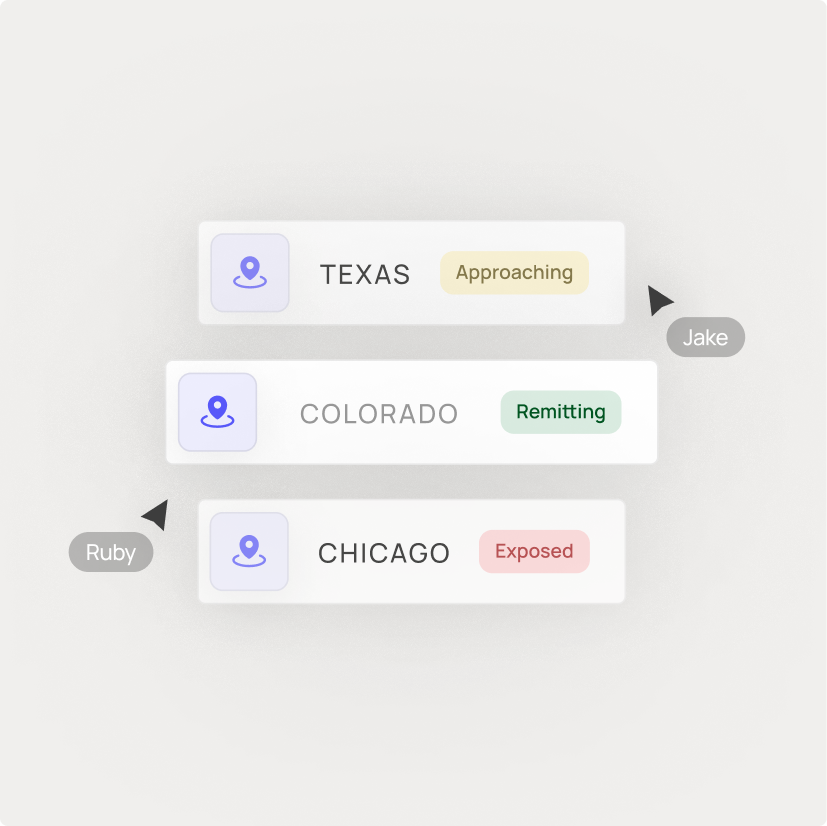

- Monitor your exposure: Track each new jurisdiction where your product is taxed and where you have customers. Each will have its own specific tax laws to take into account. A sales tax platform can automate this process for you by integrating with your billing systems, and notifying you of any potential liabilities.

- Update your TOS for tax liability: Ensure that your Terms of Service include the right contractual language so that your customer contracts are clear that your pricing does not include sales tax, and that your customer will be required to pay for any sales tax charges that do apply.

Hiring remotely

As your team grows, any new remote employees or contractors have the potential to create tax obligations. Keep track of employee locations and start dates, and compare against local tax laws to assess your exposure (or use an automated solution to monitor this for you by integrating with your HR system).

Hitting a tax threshold

Beyond employee locations, you can also trigger tax obligations by selling to customers in a country, state, or even city. Every jurisdiction has its own thresholds for requiring a business to collect sales tax or VAT. In the US, it’s typically a combination of sales amount (like $100,000) and volume (like 200 transactions), while internationally the type of transaction (B2B or B2C) often comes into play.

When you’re getting close to a new threshold—like making $100,000 in a SaaS-taxing state or selling B2C internationally—make sure you have a process or tax solution in place to handle registration and compliance in the relevant jurisdictions.

You’ll also need to prepare your business and customers for the logistics of collecting tax. Work with your executive team to get buy-in and update relevant processes across the sales and product organizations.